Yesterday, SB 648 by Sen. Yvonne Dorsey-Colomb (D-Baton Rouge) came out of the Senate Committee on Revenue and Fiscal Affairs. If passed, it would continue the long practice of Baton Rouge’s “downtown crowd” to favor “connected” investors developing property in geographical areas favored by the power elite.

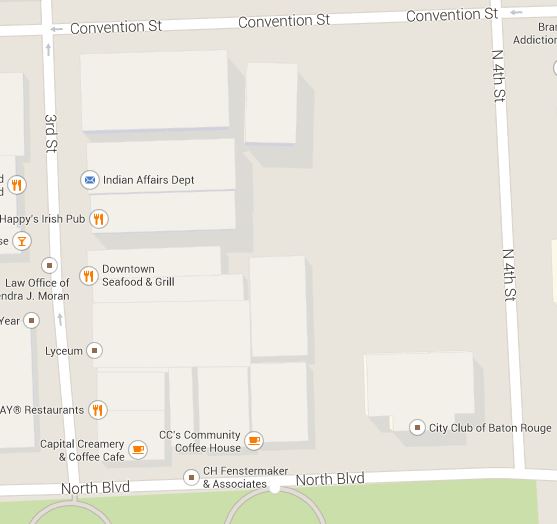

SB 648 establishes a special taxing district in a one-block area between North Boulevard and Convention Street, and 3rd and 4th Streets in downtown Baton Rouge. A Google map of the area in question…

It’s the building in the top left corner of that map which is of specific interest to the bill’s authors…

The building has an interesting history, one which has gotten even more interesting lately. It was originally built to house the Louisiana National Bank in the 1920’s, but as you can see from the sign in the front it’s been the State Office Building for quite a while. Currently, there are no state offices in the building.

Which is why the recent – very recent, in fact – history of the building is of concern here.

In January, the state sold the building for $10.2 million to the Baton Rouge Area Foundation as part of an asset dump intended to shore up a budget deficit.

And in February, BRAF sold the building to real estate developer Mike Wampold. The Baton Rouge Business Report had a blurb on that sale which revealed some peculiar information…

He tells Daily Report that he’s planning to turn the art deco-era building into either a residential development or a boutique hotel. “It was built in 1926 and has hand-painted murals throughout the first floor,” says Wampold. “It could be a really neat apartment building or a hotel or condos. We’re going to study the building and the market and see where things appear to be heading 24 or 36 months from now.”

And just a bit more…

At the time of the acquisition, BRAF said very little about its plans for the building, which, it is now apparent, included Wampold. Wampold declines to discuss the sale price, explaining that the deal was structured through BRAF because he intends to put the building, once improved, into a support foundation he established through BRAF in the name of his grandfather. “This is really a charitable endeavor,” he says. “When the hotel or whatever is developed, it will be placed in the Milford Wampold Charitable Foundation and all proceeds and profits will go to the benefit of that foundation.”

Two months later, we have a bill creating a TIF district for the hotel/apartment building project Wampold says is going into a charitable foundation under BRAF’s wing.

And the bill to create the TIF creates some mighty wide latitude as to its governance and future…

D. Governance.

(1) In order to provide for the orderly development of the district and effectuation of the purposes of the district, the district shall be administered and governed by a board of commissioners, referred to in this Section as the “board”, comprised of three persons as follows:(a) The mayor-president of the city-parish or his designee.

(b) The mayor-president pro-tempore of the city-parish or his designee.

(c) The council member for Metropolitan Council District No. 10 of the city-parish or his designee.(2) A majority of the members of the board shall constitute a quorum for the transaction of business. The board shall keep minutes of all meetings and shall make them available for inspection through the board’s secretary-treasurer. The minute books and archives of the district shall be maintained by the board’s secretary-treasurer. The monies, funds, and accounts of the district shall be in the official custody of the board.

(3) The board shall adopt bylaws and prescribe rules to govern its meetings. The members of the board shall serve without salary or per diem and shall be entitled to reimbursement for reasonable, actual, and necessary expenses incurred in the performance of their duties.

(4) The domicile of the board shall be established by the board at a location within the district.

(5) The board shall elect from its own members a president, vice president, and a secretary-treasurer, whose duties shall be common to such offices or as may be provided by bylaws adopted by the district. The board shall hold regular meetings and may hold special meetings as provided in the bylaws. The failure of the board to hold any regular meeting shall not impair any existing obligations of the district. All such meetings shall be public meetings subject to the provisions of R.S. 42:11, et seq.E. Rights and powers. The district, acting by and through its board, shall be a special taxing district and shall have and exercise all powers of a political subdivision and special taxing district necessary or convenient for the carrying out of its objects and purposes including but not limited to the following:

(1) To sue and to be sued.

(2) To adopt bylaws and rules and regulations.

(3) To receive by gift, grant, donation, or otherwise any sum of money, property, aid, or assistance from the United States, the state of Louisiana, or any political subdivision thereof, or any person, firm, or corporation.

(4) For the public purposes of the district, to enter into one or more contracts, agreements, or cooperative endeavors with the state and its political subdivisions or political corporations, the city-parish, the owners of property in the district, and with any public or private association, corporation, business entity, or person, including but not limited to a cooperative endeavor agreement, a pledge and collateral assignment agreements, and tax collection agreement.

(5) To appoint officers, agents, and employees, prescribe their duties, and fix their compensation.

(6) To acquire by gift, grant, purchase, lease, or otherwise such property as may be necessary or desirable for carrying out the objectives and purposes of the district and to mortgage and sell such property.

(7) In its own name and on its own behalf to incur debt and to issue bonds, notes, certificates, and other evidences of indebtedness, and in the event the district elects to issue bonds pursuant to the authority under this Section, then the district shall be deemed and considered to be an issuer for purposes of R.S. 33:9037, and shall, to the extent not in conflict with this Section, be subject to the provisions of R.S. 33:9037.

(8) To establish such funds or accounts as are necessary for the conduct of the affairs of the district.

(9) To levy and collect the taxes authorized pursuant to this Section.

(10) To pledge the district tax collections and other funds and property as security for the financing or refinancing of any costs incurred or to be incurred in connection with any project or projects, or parts thereof, within the boundaries of the district.

(11) To enter into one or more agreements to provide for the collection of the taxes collected within the district and remittance of the taxes to the appropriate recipients.

(12) To exercise any and all of the powers granted to an economic development district as if the district were an economic development district established pursuant to Part II of Chapter 27 of Title 33 of the Louisiana Revised Statutes of 1950, including but not limited to the powers of tax increment financing pursuant to R.S. 33:9038.33 and 33:9038.34 and the power to levy taxes within the district pursuant to R.S. 33:9038.39, provided that any such powers exercised by the district shall be subject to the provisions of Part II of Chapter 27 of Title 33 of the Louisiana Revised Statutes of 1950 unless such provisions are inconsistent with the provisions of this Section, in which case the provisions of this Section shall control.

(13) To exercise any and all of the powers granted to a community development district as if the district were a community development district established pursuant to Chapter 27-B of Title 33 of the Louisiana Revised Statutes of 1950, including but not limited to the power to levy special assessments on property within the district pursuant to R.S. 33:9039.29, provided that any such powers exercised by the district shall be subject to the provisions of Chapter 27-B of Title 33 of the Louisiana Revised Statutes of 1950 unless such provisions are inconsistent with the provisions of this Section, in which case the provisions of this Section shall control.

Those are some rather bilious and wide-ranging powers, and the bill doesn’t set much in the way of limits for the TIF district to eventually expand out of the box it’s being created in.

In fact, if you were going to consider this thing as a blob which might well eat all of downtown Baton Rouge there are people who would agree with you.

Notice also that the bill establishes a three-person governing board of the taxing district in question, which would include mayor-president Kip Holden, Baton Rouge mayor pro tempore Chandler Loupe and Metro Councilwoman Tara Wicker, or their designates. That looks an awful lot like a constant 2-1 vote where Loupe gets outvoted on all kinds of decisions which could have major importance to what properties in downtown Baton Rouge get swallowed up for favorable treatment on behalf of their developers…assuming the developers are connected with the right people.

In fact, it wouldn’t be all that out of line to wonder if this thing couldn’t eventually grab every currently-unused piece of land in downtown Baton Rouge so as to redevelop those properties under the TIF model – so long as friendly developers can be found to benefit from the financing.

Mike Wampold, whose reputation as a real-estate developer is outstanding and who has been responsible for bringing to life some of Baton Rouge’s best property, doesn’t need a TIF to finance the old LNB building into a hotel – and one could ask why, with four hotels in downtown Baton Rouge it’s necessary to put tax dollars at risk to finance the fifth. Wampold could certainly afford to put his own money at risk on this project.

And Baton Rouge doesn’t need to create a TIF to finance a fifth downtown hotel. It will be said that the first four hotels in downtown Baton Rouge were all financed with TIF’s, and that’s true. But at the time those hotels were financed, Baton Rouge didn’t have enough downtown hotel space to compete in the convention business. At what point is there no longer a public-policy need for hotels in downtown Baton Rouge sufficient for taxpayers to be on the hook for the financing?

And who will ever build a hotel in downtown Baton Rouge again without demanding that taxpayer-backed bonds fund their project?

For that matter, who will ever seek to build anything in downtown Baton Rouge without TIF financing? Consider this – we’re supposed to believe that somebody without political connections is going to put down millions of dollars to develop property in downtown Baton Rouge, in the knowledge that if his idea has merit the folks with political connections might very well jump in with their own investors, who are able to use BRAF either as a straw purchaser for land or some sort of partner giving their project a non-profit cover and then apply a TIF to finance their project, to compete against him.

In practice, nobody will do that. In practice, a bill like this will consolidate the property of downtown Baton Rouge in the hands of a connected elite. In practice, the only people who will develop property downtown will be people who know the mayor and the Powers That Be, and who can suitably kiss their rings.

Winners and losers will be chosen.

This isn’t the free market. This is a dangerous bill.

Advertisement

Advertisement