The story goes that several years ago an elderly pastor knew the end was near, so he summoned his legislator and his lawyer, both members of his church. The immediately came, and the pastor motioned for them to sit on either side of his bed. He stretched out his hands, and grasped theirs, sighed contentedly, and waited for the end. After several hours, the legislator spoke up: “Pastor, we appreciate you inviting us to be here, and we are very sorry for your health. But why did you want us to come?”

The pastor gently replied: “Jesus died between two thieves, so I figured I ought to go out the same way.”

If the pastor died today, the legislator would most likely have his hands in the pastor’s pocket. For it turns out that the Legislature of Louisiana, that august body of men and women gathered from across the state to protect our rights, a majority of which identify as Republicans, the Louisiana boys and girls of summer, passed a tax on churches and other non-profits during the 2015 session.

Let’s recap the details, as laid out by my colleague Kevin Boyd:

- The business utility sales tax exemption was cut by 25%.

- The cigarette tax was increased $0.50 and vaping products were included.

- Most exemptions and credits were whacked 20% across the board.

- Corporate tax incentives were whacked 28% across the board.

- Car titles will go up from $18 to $68.

- There were tax increases dealing with out of state taxes and corporate tax credits.

- As a small consolation, all the tax hikes, except for the cigarette tax hike, will sunset after 3 years.

I know what you’re thinking: “I don’t see any taxes on churches, unless the church is paying for the pastor’s cigarettes.” Ah, the devil is in the details.

Louisiana, as a general rule, taxes the sale of all consumables, like water, electricity, and natural gas. The reason we seldom pay taxes on these things is because of the myriad of tax exemptions. For instance, the Constitution of Louisiana, Art. 7, Sec. 2.2 provides a rock-solid exemption for residential users of those items:

Effective July 1, 2003, the sales and use tax imposed by the state of Louisiana or by a political subdivision whose boundaries are coterminous with those of the state shall not apply to sales or purchases of the following items:

(1) Food for home consumption, as defined in R.S. 47:305(D)(1)(n) through (r) on January 1, 2003.

(2) Natural gas, electricity, and water sold directly to the consumer for residential use.

(3) Prescription drugs.

Note that the constitutional exemption for natural gas, electricity, and water is ONLY for RESIDENTIAL use. Thus, my meager law firm, not being a residence (although I feel like I live here most of the time), does not qualify under the constitution for an exemption.

Never fear, though, as the Legislature several years ago passed an exemption from sales taxes for natural gas, electricity, and water:

The sale at retail, the use, the consumption, the distribution, and the storage to be used or consumed in the taxing jurisdiction of the following tangible personal property is hereby specifically exempted from the tax imposed by taxing authorities, except as otherwise provided in this Paragraph:

(b) Steam.

(c) Water (not including mineral water or carbonated water or any water put in bottles, jugs, or containers, all of which are not exempted).

(d) Electric power or energy and any materials or energy sources used to fuel the generation of electric power for resale or used by an industrial manufacturing plant for self-consumption or cogeneration.

(g) Natural gas.

Then, this year the Legislature changed their mind.

This year, through HCR 8, the Legislature suspended the statutory exemption: “THEREFORE,BE IT RESOLVED that the Legislature of Louisiana hereby suspends all of the exemptions from the tax levied pursuant to R.S. 47:331 for sales of steam, water, electric power or energy, and natural gas….”

Just to make sure we’re all on the same page, let’s recap:

- The constitution exempts from sales tax natural gas, electricity, and water used for residential purposes.

- State statute exempts from sales tax natural gas, electricity, and water (and steam) used for any purposes.

- The Legislature suspended the statutory exemption but could not suspend the constitutional exemption.

Thus, the only sales tax exemption on natural gas, electricity, and water in place after the 2015 session is the constitutional exemption which, as noted above, only exempts residential users. In other words, if your not a residential user of natural gas, electricity, and water, the tax man cometh. Churches, fraternities, and other non-profit organizations all get to pay sales tax on natural gas, electricity, and water because they’re not residential users.

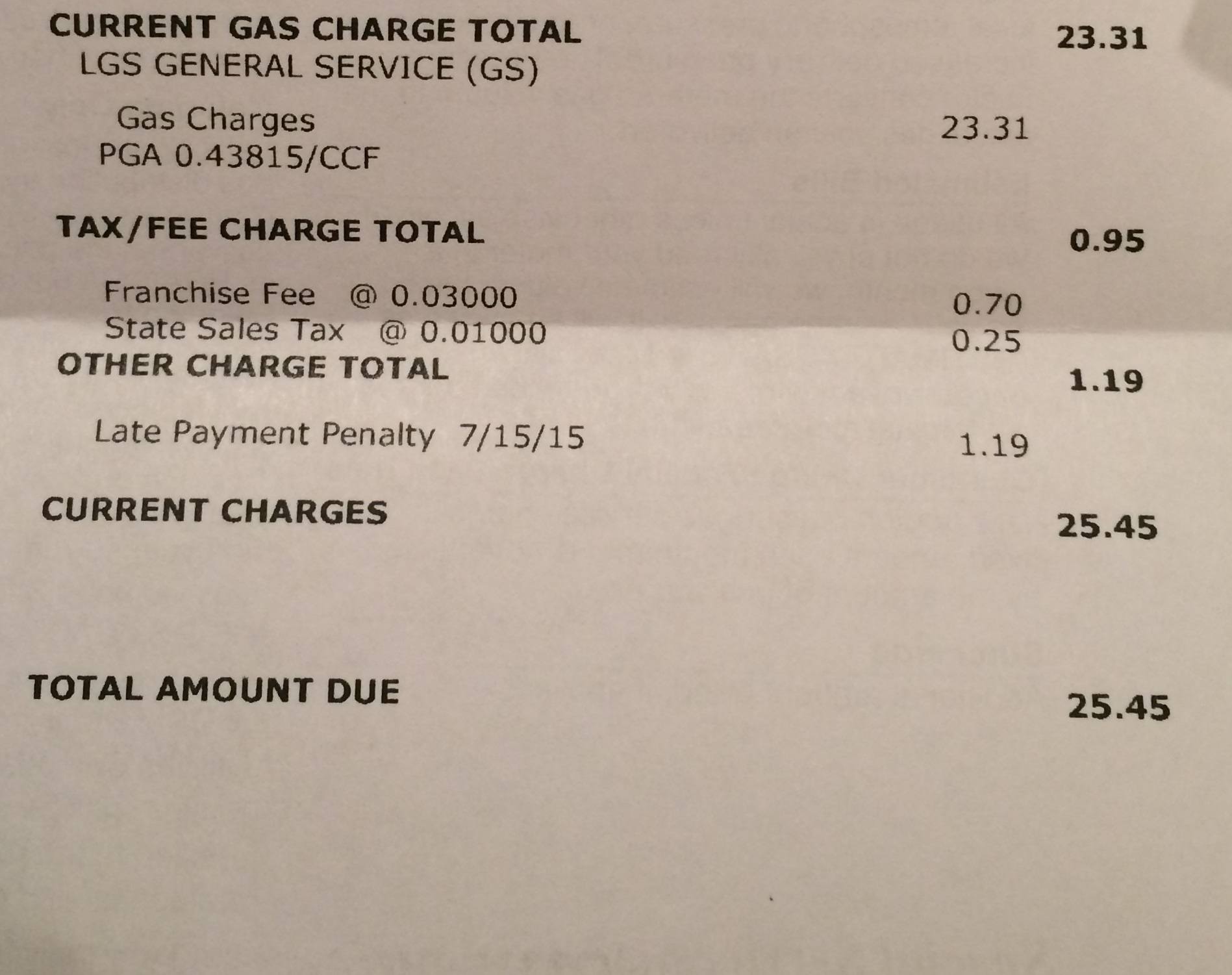

Which is why a local non-profit got the following in their water and gas bills:

The boys and girls of summer in our Legislature told us this was a “business tax.” Pull up the bill on the Legislature’s website and it will tell you it’s a tax on businesses. Businesses are up in arms about it. But this is not just a business tax. This is a tax on ALL non-residential users of natural gas, electricity, and water.

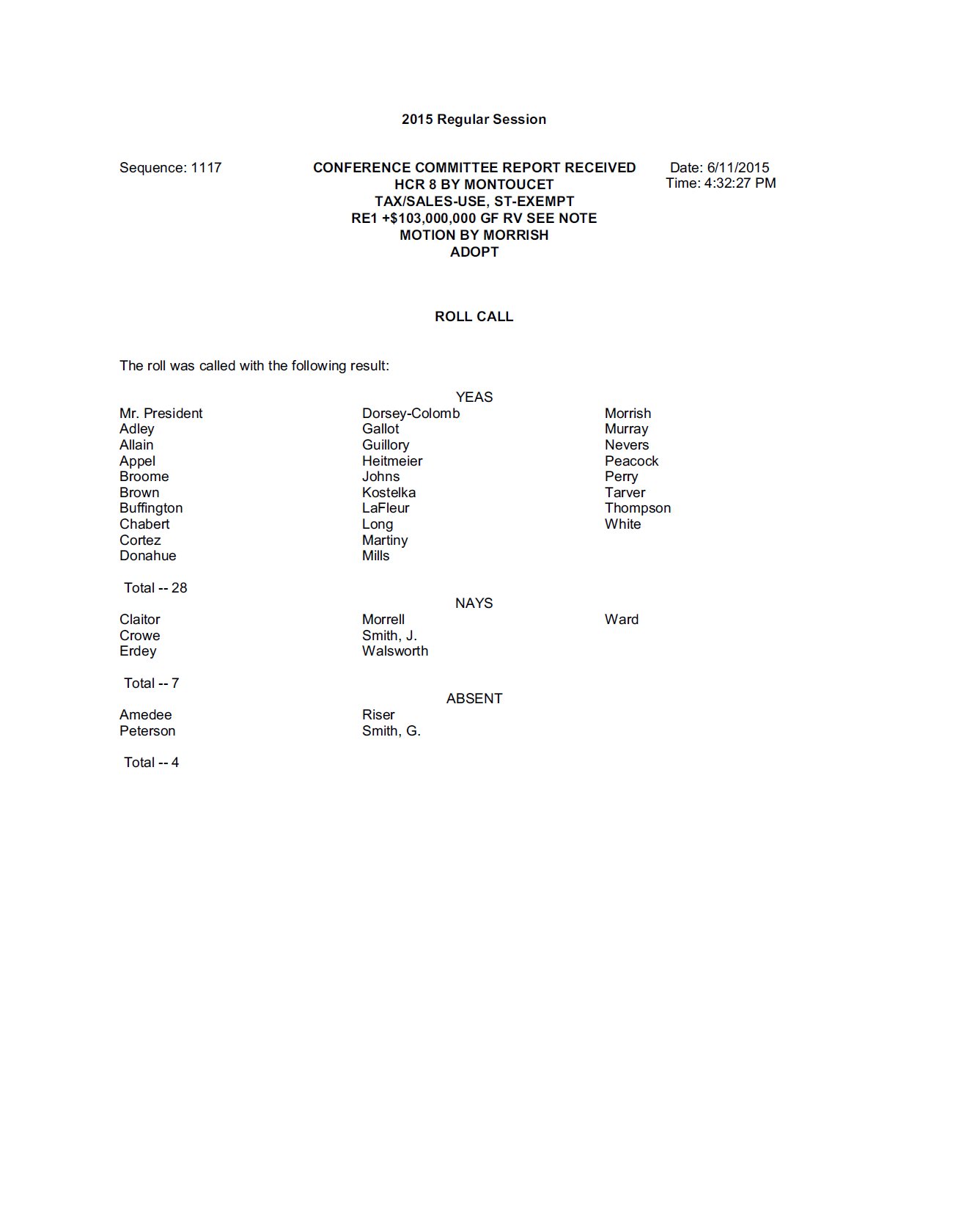

Of course, I’d be remiss unless I reminded you which House and Senate members voted in favor of the church tax:

This is exactly why we should hold our legislators accountable. In an effort to tax their way into prosperity, the Legislature went all willy-nilly raising taxes on disfavored groups and failed to fully study just who they were raising taxes on. The idea to tax should be studied CAREFULLY and only after much thought and only as a last resort should tax measures be enacted. The Legislature apparently didn’t do that here, and Louisiana’s non-profit organizations get to pay for it, literally.

Advertisement

Advertisement